Page 66 - MA - May 2017

P. 66

FINANCIAL MANAGEMENT

In which purposes (motivating factors), derivative instruments are used?

In this question, we tried to seek answers about the nature of risks hedged such as fluctuations in accounting

earnings, fluctuations in cash flows, balance sheet ratios, market value of the firm, etc. by the corporate in India.

We asked the respondents to rank the nature of risks hedged in a four-point ranked scale.

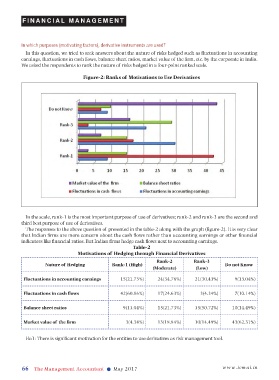

Figure-2: Ranks of Motivations to Use Derivatives

In the scale, rank-1 is the most important purpose of use of derivatives; rank-2 and rank-3 are the second and

third best purpose of use of derivatives.

The responses to the above question of presented in the table-2 along with the graph (figure-2). It is very clear

that Indian firms are more concern about the cash flows rather than accounting earnings or other financial

indicators like financial ratios. But Indian firms hedge cash flows next to accounting earnings.

Table-2

Motivations of Hedging through Financial Derivatives

Rank-2 Rank-3

Nature of Hedging Rank-1 (High) Do not Know

(Moderate) (Low)

Fluctuations in accounting earnings 15(21.73%) 24(34.78%) 21(30.43%) 9(13.04%)

Fluctuations in cash flows 42(60.86%) 17(24.63%) 3(4.34%) 7(10.14%)

Balance sheet ratios 9(13.04%) 15(21.73%) 35(50.72%) 10(14.49%)

Market value of the firm 3(4.34%) 13(18.84%) 10(14.49%) 43(62.31%)

Ha1: There is significant motivation for the entities to use derivatives as risk management tool.

66 The Management Accountant l May 2017 www.icmai.in