Page 119 - MA - May 2017

P. 119

Resource costs

Direct Indirect

Indirect cost allocation based on resource consumption Resource drivers

Costs of

transportation activities

Direct cost allocation Activity cost allocation based on performance consumption cost drivers

Production cost

of elementary transportation services

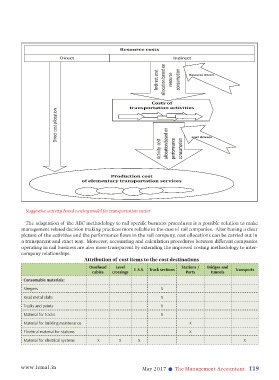

Suggestive activity based costing model for transportation sector

The adaptation of the ABC methodology to rail specific business procedures is a possible solution to make

management related decision making practices more reliable in the case of rail companies. After having a clear

picture of the activities and the performance flows in the rail company, cost allocations can be carried out in

a transparent and exact way. Moreover, accounting and calculation procedures between different companies

operating in rail business are also more transparent by extending the improved costing methodology to inter-

company relationships.

Attribution of cost items to the cost destinations

Overhead Level E.S.S. Track sections Stations / Bridges and Transports

cables crossings Ports tunnels

Consumable materials:

Sleepers X

Road metal-slabs X

Tracks and points X

Material for tracks X

Material for building maintenance X

Electrical material for stations X

Material for electrical systems X X X X

www.icmai.in May 2017 l The Management Accountant 119