Page 118 - MA - May 2017

P. 118

FROM THE RESEARCH DESK

- transport x x x X x

engine

- transport x x x X x

equipment

- transport

workshop X x x x

machines

- ticket x

machines

#parameters may vary according to the sectors

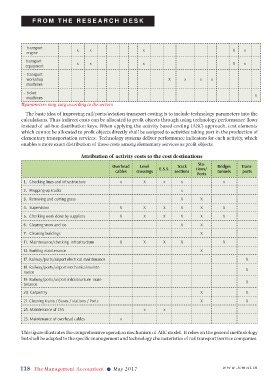

The basic idea of improving rail/ports/aviation transport costing is to include technology parameters into the

calculations. Thus indirect costs can be allocated to profit objects through using technology performance flows

instead of ad-hoc distribution keys. When applying the activity based costing (ABC) approach, cost elements

which cannot be allocated to profit objects directly shall be assigned to activities taking part in the production of

elementary transportation services. Technology systems deliver performance indicators for each activity, which

enables a more exact distribution of these costs among elementary services as profit objects.

Attribution of activity costs to the cost destinations

Sta-

Overhead Level E.S.S. Track tions/ Bridges Trans-

cables crossings sections tunnels ports

Ports

1. Checking lines and infrastructure x X x x x

2. Propping up tracks x

3. Removing and cutting grass X X

4. Supervision X X X X X X

5. Checking work done by suppliers X X X X X X

6. Clearing snow and ice X X

7. Cleaning buildings X

11. Maintenance/checking infrastructure X X X X X

13. Building maintenance X

17. Railway/ports/airport electrical maintenance X

18. Railway/ports/airport mechanical mainte-

nance X

19. Railway/ports/airport infrastructure main- X

tenance

20. Carpentry X X

21. Cleaning trains / Buses / stations / Ports X X

23. Maintenance of ESS x x

25. Maintenance of overhead cables x

This figure illustrates the comprehensive operation mechanism of ABC model. It relies on the general methodology

but shall be adapted to the specific management and technology characteristics of rail transport/service companies.

118 The Management Accountant l May 2017 www.icmai.in